How To Prepare for Student Loan Payments

After you graduate, drop below half-time enrollment, or leave school, your federal student loan(s) go into repayment. If you have a Direct Subsidized Loan or a Direct Unsubsidized Loan, you’ll have a six-month grace period before you’re required to start making monthly payments. If you’re exiting a temporary payment pause, such as a deferment or forbearance, you’ll have a window between when the notice is sent and when you’re required to continue making monthly payments.

Use this time to prepare for your upcoming payments with these steps:

- Get information about your student loan account.

- Explore repayment plans.

- Take action if you want to lower your monthly payment.

- Enroll in auto pay.

- As a last resort, contact your loan servicer to ask for short-term relief.

- Understand what happens if you don’t repay your loan.

1

Get information about your student loan account.

When your student loan was first disbursed (paid out), you were assigned a student loan servicer. Your servicer handles billing and other services related to your federal student loan, including helping you explore and understand repayment options.

Make sure your contact information is up to date in your profile on your loan servicer’s website and your StudentAid.gov account settings. Incorrect contact information could make you miss important updates about upcoming payments.

Before your payment is due, your loan servicer(s) will send you a billing statement or other notice. This notice will include

- your payment due date,

- your upcoming interest,

- your payment amount, and

- how to access your loan information and make a payment on their website.

Your payment will be due no sooner than 21 days after your loan servicer sends the billing statement.

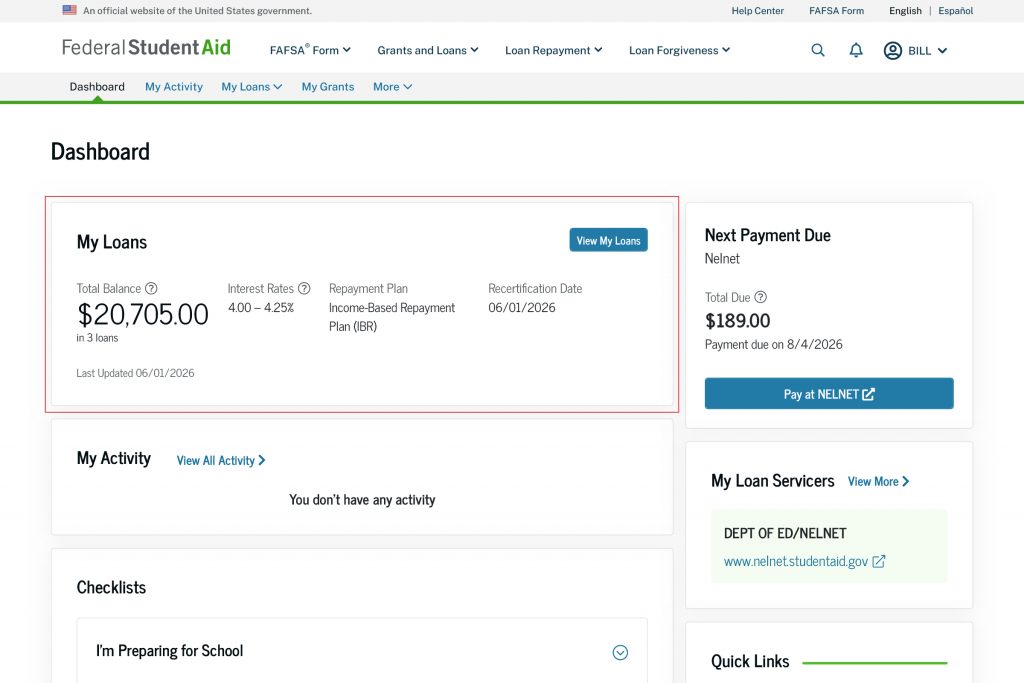

You’ll also be able to see your loan information when you log in to your StudentAid.gov account Dashboard. This includes your total balance, interest rate, current repayment plan, next payment due date, next payment amount due, and a link to pay on your loan servicer’s website. Your account Dashboard is a helpful tool for managing and tracking your payments.

| Student Loan Servicer | Website | Phone Number |

|---|---|---|

| Edfinancial | edfinancial.StudentAid.gov | 1-855-337-6884 |

| MOHELA | mohela.StudentAid.gov | 1-888-866-4352 |

| Aidvantage | aidvantage.StudentAid.gov | 1-800-722-1300 |

| Nelnet | nelnet.StudentAid.gov | 1-888-486-4722 |

| ECSI | efpls.ed.gov | 1-866-313-3797 |

| Default Resolution Group | myeddebt.ed.gov | 1-800-621-3115 |

| CRI | cri.StudentAid.gov | 1-833-355-4311 |

2

Explore repayment plans.

After you leave school—if you don’t choose to enroll in another repayment plan—you’ll automatically be enrolled in the Standard Plan or Tiered Standard Plan (depending on when your student loans were first disbursed). However, most borrowers can switch to a repayment plan based on their income.

An income-driven repayment (IDR) plan calculates your monthly payment amount based on how much money you make and your family size. Under an IDR plan, payments can be as low as $10 per month. Note that you might have limited access to certain repayment plans, depending on when your loan was first disbursed.

We also offer fixed payment repayment plans. On these plans, your monthly payment is set at an amount that ensures your loan is paid off within a predetermined length of time (the “repayment period”).

You can use our Repayment Calculator tool to explore and compare your repayment plan options. Repayment Calculator can tell you which repayment plan offers you the lowest monthly payment amount, fastest payoff, lowest total paid, and least interest paid. We recommend that you log in to your StudentAid.gov account before using Repayment Calculator. Doing so means your loan information will automatically populate in the tool.

You’ll also have the option to import your up-to-date financial information from the IRS to help make the payment amount estimates in the tool more accurate.

3

Take action if you want to lower your monthly payment.

Once you understand your repayment options and see your personalized results from Repayment Calculator, you can choose the plan that works best for you. If you decide on one, you can apply for an IDR plan online.

Is your grace period ending soon? If you’re like most borrowers in a grace period, you can apply online for an IDR plan 60 days before your grace period ends (or at any time by contacting your loan servicer). We recommend you apply early so that your first payment is under your chosen plan.

Are you exiting deferment or forbearance and are already on an IDR plan, but your income has changed (such as from a job change or layoff or if your family size has increased)? You can use the online IDR application to recalculate your monthly payment amount at any time; you don’t need to wait for your annual recertification date.

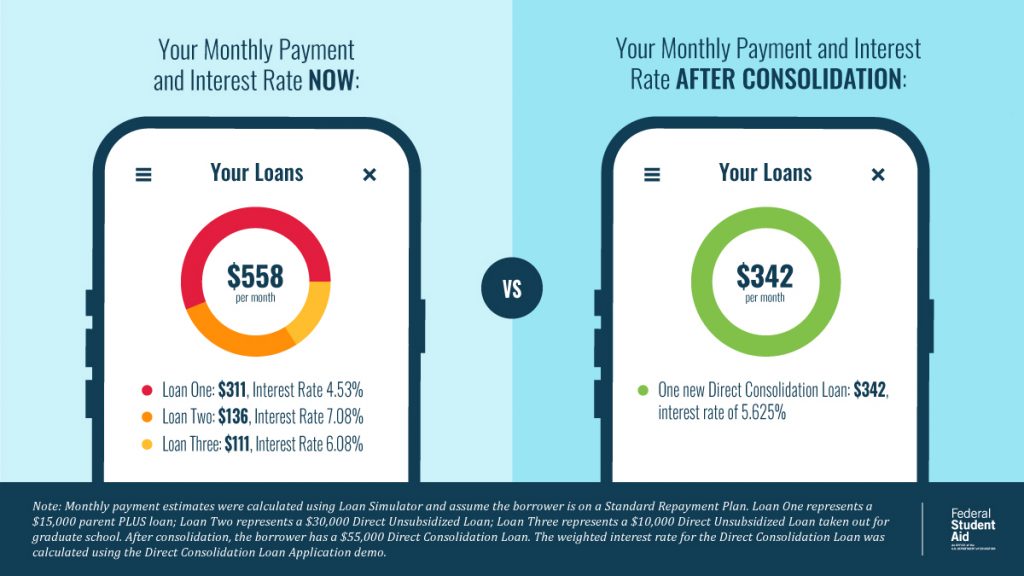

Consolidating your federal student loans is another way you can lower your monthly payments. However, you should consider the pros and cons of consolidation to decide if consolidation is right for you. If you have a Direct PLUS Loan, there might be more things to consider before choosing consolidation.

4

Enroll in auto pay.

Enrolling in auto pay means your loan servicer will automatically deduct your payment from your bank account on time each month.

On auto pay, you’ll get a reminder ahead of each withdrawal. Sign up for auto pay (for free!) on your loan servicer’s website.

Starting on July 1, 2026, federal student loan borrowers enrolled in auto pay will enjoy a 1% interest rate reduction! Borrowers enrolled in auto pay by September 30, 2026, (or those who are already enrolled) will benefit from this interest rate reduction through June 30, 2028.

5

As a last resort, contact your loan servicer to ask for short-term relief.

If you’ve applied for an IDR plan but you still can’t afford your payment, you can request to temporarily pause or lower your payments through short-term relief (deferment or forbearance). If this option makes sense for you, you should contact your loan servicer to request a deferment or forbearance.

Interest can still accrue (add up) during periods of deferment or forbearance. Deferment and forbearance can also affect loan discharge options, such as Public Service Loan Forgiveness or IDR plan discharge.

6

Understand what happens if you don’t repay your loan.

The first day after you miss a student loan payment, your loan becomes past due, or delinquent. If your loan is delinquent for 90 days or more, your loan servicer will report the delinquency to the three major national credit bureaus. Delinquency will affect your credit score, making it harder to get credit

After 270 days, your delinquent loan goes into default. When you default on a loan, here’s what happens:

- You can lose your access to more student aid.

- The default status will damage your credit score.

- To pay off your defaulted loan, the government can take your tax refund, part of your Social Security benefits, or up to 15% of your paycheck.

Read our “Student Loan Default and Collections: FAQs” article to learn how default works and what your options are if you default on your student loan(s).

Other Resources

- “Repaying Student Loans 101” page

- “How To Prep for Student Loan Repayment” video

- “Top FAQs About Income-Driven Repayment Plans” article

- “Compare Student Loan Repayment Plans With Our Student Loan Calculator” article

- “Student Loan Borrower Q&A” section of the “IDR Plan Court Actions” page

- “One Big Beautiful Bill Act Updates” page

Published: July 2026