How To Avoid Student Loan Forgiveness Scams

Student loan forgiveness calls, emails, or text messages setting off your scam sensors? Read on to learn how to identify and avoid student loan forgiveness scams and find out what you should do if you think you’ve been scammed.

Scams come in all shapes and sizes, from phone calls and emails to text messages. You may encounter scams tied to current events. But sometimes it’s as simple as a fake promise to work fast and save you lots of money. Remember: A scam doesn’t have to be elaborate or complex.

The Federal Trade Commission received 2.6 million fraud reports in 2023.

There are legitimate programs and resources available if you need help with your federal student loans, including the

- Federal Direct Consolidation Loan Program,

- Public Service Loan Forgiveness (PSLF) Program, and

- Teacher Loan Forgiveness Program.

You can work with your loan servicer to explore which options may be right for you—free of charge. For specific questions about PSLF, contact the Federal Student Aid Information Center (FSAIC).

Many companies will try to take advantage of borrowers by guaranteeing immediate results or requesting money up front for services they can’t provide.

What do common scams look like?

Aggressive Advertising Language

Here are some examples of false claims you might come across:

- “Act immediately to qualify for student loan forgiveness before the program is discontinued.”

- “Your student loans may qualify for complete discharge. Enrollments are first come, first served.”

- “Student alerts: Your student loan is flagged for forgiveness pending verification. Call now!”

Although the U.S. Department of Education may reach out to highlight temporary programs, aggressive advertising language like the above will not come from us or our partners.

Promises That Are Too Good To Be True

Scammers will frequently request an up-front or monthly fee while promising immediate and total student loan cancellation. Most government forgiveness programs require years of qualifying payments and/or employment in certain fields before forgiving loans.

Requests for Log-In Info

A scammer may even ask for your StudentAid.gov account information, like your account username and password. This is a red flag. We and our partners will never ask for your password. That’s a guarantee.

The U.S. Department of Education and our partners—including loan servicers—will never ask for your StudentAid.gov username and password.

Typos and Grammatical Errors

If you receive a questionable message promising student loan forgiveness and aren’t sure what to make of it, keep an eye out for any unusual capitalization, improper grammar, or incomplete sentences. These sorts of errors indicate a potential scam in action.

Unofficial Addresses or Phone Numbers

Some scammers may use official-looking names, seals, and logos, but that doesn’t make them trustworthy. Know what official communications from us and our partners look like and always double check the sender’s email address.

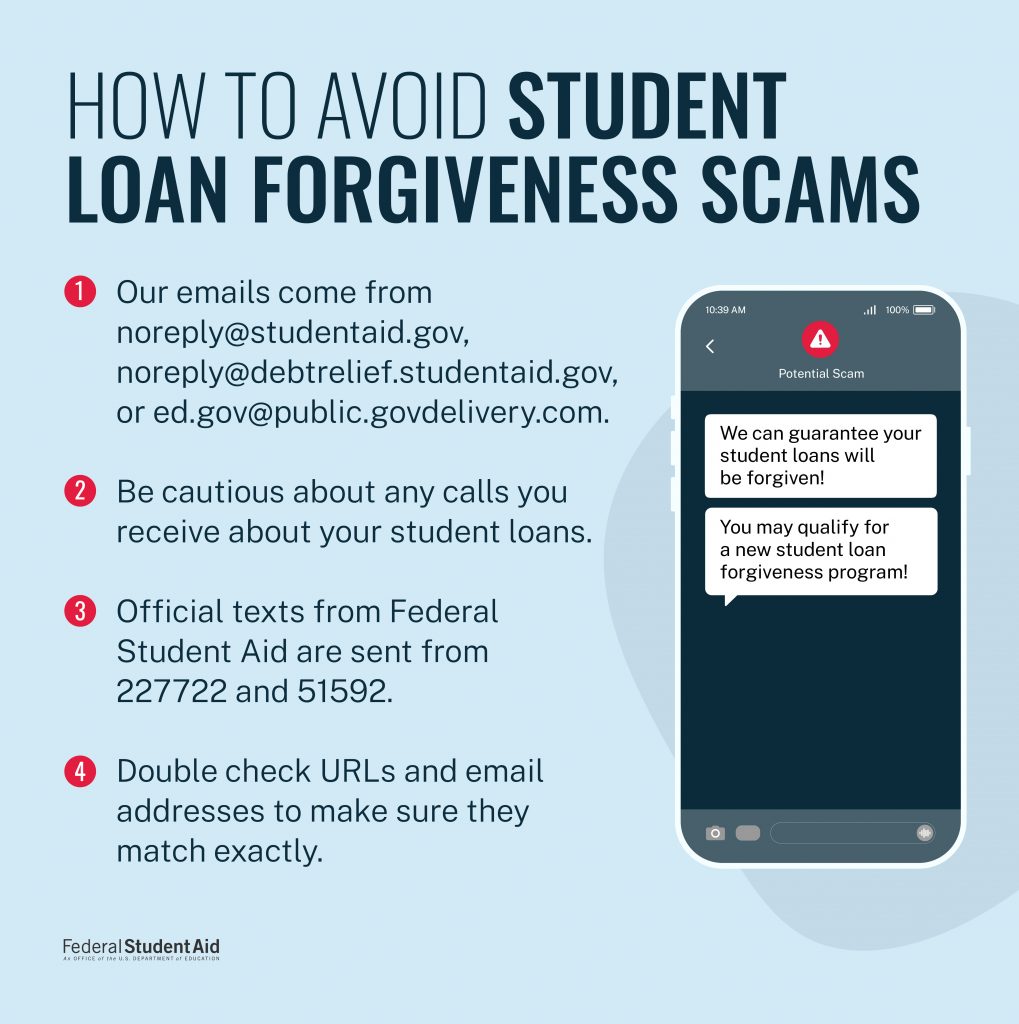

Emails from us will only come from these addresses:

Text messages from us will only come from 227722 or 51592.

Still not sure if you’re being scammed? You can check with your local Better Business Bureau® to see if a company has any complaints.

Who are legitimate loan servicers and what do they do?

We work hand in hand with some private companies—such as lenders and loan servicers—to support federal student loans and borrowers. To avoid student loan forgiveness scams, it’s important to know who these companies are and the free services they provide.

Your loan servicer works on the government’s behalf to

- collect your loan payments,

- answer any questions you have about your loans,

- help you decide which repayment plan is right for you, and

- help you switch to a new plan at no cost.

You don’t need to pay someone to help you navigate repaying your student loans or to help you reach loan forgiveness. Your loan servicer can help you get set up with the right program. And remember: our loan forgiveness programs are always free. To find out who your student loan servicer is, log in at StudentAid.gov to visit your account Dashboard. You can also call the FSAIC.

If you need help with your federal student loans or are pursuing some form of student loan forgiveness, make sure you’re contacting a U.S. Department of Education affiliated company that you can trust (our official loan servicers use websites and email addresses ending in .gov). Review our list of contracted federal student loan servicers before reaching out to a potential partner.

| Loan Servicer | Contact |

|---|---|

| Aidvantage | aidvantage.StudentAid.gov |

| CRI | cri.StudentAid.gov |

| Default Resolution Group | myeddebt.ed.gov |

| ECSI | efpls.ed.gov |

| Edfinancial | edfinancial.StudentAid.gov |

| MOHELA | mohela.StudentAid.gov |

| Nelnet | nelnet.StudentAid.gov |

Should I pay for debt relief help?

If you’re having difficulty paying for your student loans, your first step should be to contact your loan servicer. Some debt relief companies will charge a fee for services that you and your servicer can work out together, for free.

We and our affiliated federal loan servicers can help you

- lower your monthly loan payment,

- consolidate multiple federal student loans,

- switch to a new repayment plan, or

- see if you qualify for loan forgiveness.

Getting assistance from a private, unaffiliated debt relief company doesn’t necessarily mean you’ll be scammed. But seeking out unverified services is a common path to a student loan forgiveness scam.

What should I do if I think I’ve been scammed?

For all types of student loan forgiveness scams, act fast and follow one or all of these options:

- Contact your federal loan servicer to make sure no unwanted actions were taken on your loans (or to revoke any authorization agreement that your servicer has on file).

- Contact your bank or credit card company to stop all payments to the company that is scamming you.

- Submit a complaint to us.

- File a complaint with the Federal Trade Commission.

- File a complaint with the Consumer Financial Protection Bureau.

StudentAid.gov Account Scams

If you find yourself involved in a scam that concerns your StudentAid.gov account, or if you’ve shared your account username and password details with someone whom you now suspect to be a scammer, be sure to log in and change your password as soon as possible. You should also check your account information (contact email, address, and phone number) to make sure it’s still accurate. Lastly, you should file a complaint, so we can monitor your account for continued suspicious activity. Again, the U.S. Department of Education and our partners will never ask for your StudentAid.gov account username or password.