Student Loan Forgiveness (and Other Ways the Government Can Help You Repay Your Loans)

The U.S. Department of Education is implementing significant changes to the federal student aid programs. We are working to update StudentAid.gov to reflect those changes. In the meantime, stay current on these big updates.

You may be able to get help repaying your loans, including full loan forgiveness, through other federal student loan programs.

This article will cover forgiveness and discharge options related to:

- Income-Driven Repayment (IDR) Plans

- Public Service Loan Forgiveness (PSLF)

- School-Related Discharge Options

- Teacher Loan Forgiveness

- Total and Permanent Disability (TPD) Discharge

- Military Service

- AmeriCorps

1

Income-Driven Repayment (IDR) Plans

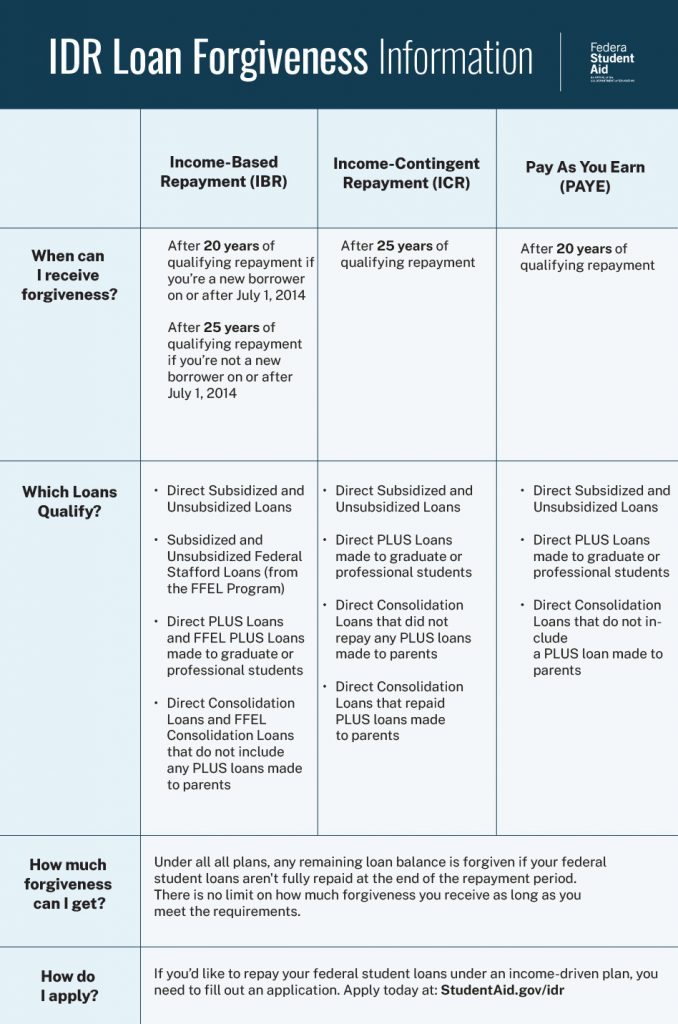

An IDR plan bases your monthly payment on your income and family size. If you repay your loans under an IDR plan, the end of term balance on your student loans may be forgiven after you make a certain number of payments over 20 or 25 years (240 or 300 monthly payments).

Use Loan Simulator to compare plans, estimate monthly payment amounts, and see if you’re eligible for an IDR plan.

Your IDR repayment period and monthly payment amount depend on which IDR plan you’re eligible to choose from.

See below for a quick comparison of the plans. Ready to apply? Apply for an IDR plan now.

2

Public Service Loan Forgiveness (PSLF)

If you work full time for a government or not-for-profit organization, you may qualify for forgiveness of the entire remaining balance of your Direct Loans

- after you’ve made 120 qualifying monthly payments under a qualifying repayment plan, and

- while working full-time for an eligible employer.

To benefit from PSLF, you need to repay your federal student loans under an IDR plan or a standard 10-year plan.

New to PSLF? Check out our “4 Beginner Tips for Public Service Loan Forgiveness Success.”

If you’re interested in PSLF, use the PSLF Help Tool to apply.

3

School-Related Discharge Options

Borrower defense to repayment is a legal ground for discharging federal Direct Loans. Borrowers apply for borrower defense for specific reasons that are outlined more thoroughly here. Another form of school-related discharge is closed school discharge. If your school closes while you’re enrolled or soon after you withdraw, you may be eligible for discharge of your federal student loan if you meet certain requirements.

4

Teacher Loan Forgiveness (TLF)

You may be eligible for forgiveness of up to $17,500 if you teach full time for five complete and consecutive academic years in certain elementary or secondary schools or educational service agencies that serve low-income families, and if you meet other qualifications. Learn more about Teacher Loan Forgiveness.

Remember, you may not receive a benefit under both the TLF Program and the PSLF Program for the same period of teaching service.

For more resources for teachers, check out our article, “4 Loan Forgiveness Programs for Teachers.”

5

Total and Permanent Disability (TPD) Discharge

To get TPD discharge, you must have a disability that severely limits your ability to work, now and in the future. This can be a physical or a mental disability. If you get a TPD discharge, you don’t have to repay any of your federal student loan(s) or complete your Teacher Education Assistance for College and Higher Education (TEACH) Grant service obligation.

In most cases, you’ll have to provide specific kinds of proof of your disability and may be subject to a post-discharge monitoring period which could reinstate your discharged loans. But some people get an automatic discharge if they are identified as eligible by the Social Security Administration or Veterans Affairs. Learn about how to qualify and apply for TPD discharge online.

6

Military Service

The U.S Department of Education and Department of Defense have special benefits for military service members with federal student loans. Benefits include interest rate caps under the Servicemembers Civil Relief Act and Department of Defense student loan repayment programs.

In addition, your military service can also count toward PSLF.

Find more information about these benefits at StudentAid.gov.

7

AmeriCorps

The Segal AmeriCorps Education Award is a benefit received by participants who complete a term of national service in an approved AmeriCorps program—AmeriCorps VISTA, AmeriCorps NCCC, or AmeriCorps State and National. After you successfully complete your service, you are eligible to receive a Segal AmeriCorps Education Award, which can be used to repay qualified student loans.

AmeriCorps service can also count toward PSLF.

Still looking for more information? Check out our student loan forgiveness page for information about other types of loan forgiveness and discharge.

You never have to pay for help with your student loans. Learn how to avoid student loan forgiveness scams.